When executing a non-every-day task sometimes it can pay to go back to basics to better understand what’s needed and the right process to go through to effect the taks efficiently and effectively for the client, says Denton’s Stephen McPhillips.

Acquisition of commercial property by a self invested personal pension (SIPP) or a small self administered scheme (SSAS) is generally not something that adviser firms deal with every day. Indeed, some firms may not have encountered this form of investment for their clients before. There could, therefore, be a natural reluctance to get involved in this type of pension planning for clients; but at what price? A client eager to invest in this way might one day call and ask for the adviser’s help in sourcing a solution and that client might be disappointed if the adviser is unable to assist.

A desire to meet a client’s needs in this way is often the driver for an adviser firm to take the first steps into the world of commercial property investment through self invested pension schemes. So, how might it all work?

Why would clients invest in this way?

The first question going through an adviser’s mind might well be; why does the client want to make the purchase through a registered pension scheme?

The reasons for this could be many and varied. For example, the client may have read or heard of the substantial benefits of this type of pension scheme investment:

- the pension scheme is a separate legal entity from the client’s business and the client as an individual, meaning that assets within it are legally ring-fenced from them;

- assets in the scheme usually sit outside of the client’s estate;

- income received from the property is received tax-free into the pension scheme;

- Capital Gains Tax is not payable on eventual disposal of a scheme-owned property;

- the property might provide a stable (and possibly rising) income stream for the scheme;

- where the vendor of the property is the client or the client’s business, sale of it to the pension scheme (at an open-market value) releases capital to the client / client’s business (and that may prove to be a much-needed financial lifeline whilst still representing a good investment opportunity for the scheme)

Another reason might be the fact that the client / client’s business cannot afford to acquire the property utilising their own resources, but there is sufficient funding available through the client’s accumulated pension scheme(s). Of course, the client’s current scheme(s) may not be able to accommodate the property investment and an adviser’s advice could be invaluable in researching the market for, and recommending, a suitable provider to meet the client’s needs, as well as advising on the merits of the pension transfer / switch that would be involved.

Hence, there are strong reasons for an adviser firm to engage with clients looking to make a property acquisition through a pension scheme.

What might be the first steps?

Accepting, of course, that the adviser will not be advising on selection of the property itself, it is likely that the initial part of the process will involve the client informing the adviser that he / she has found a commercial property that meets their needs and requesting the adviser’s help in sourcing a provider that can accommodate the purchase. That might prompt an immediate review of the client’s existing pension arrangement(s) and reporting back to the client with current fund values, current transfer values, investment features within the client’s current pension scheme(s) and so on. Already, the adviser firm’s input to the process could be of significant value to the client.

The next step for the adviser firm might be consultation with a respected and experienced provider that offers a wide range of commercial property solutions – examples of these being options for outright purchase by the pension, purchase with the assistance of pension scheme borrowing, joint purchase with another party (such as the client and / or the client’s business), part-purchase and so on. As every property is unique, a “one-size-fits-all” approach may not fulfil the client’s needs and an experienced provider can often provide much-needed flexibility when it comes to property purchase.

Ideally, from the adviser’s and client’s perspectives, the provider will offer a ready-made digital commercial property questionnaire for completion, signature and return electronically, the contents of which will enable the provider to confirm a decision on the proposed purchase in principle – and in a timely manner. Also, in an ideal world, the provider will provide its in-principle decision free of charge and without obligation, so that there is no cost to the client for exploring this investment opportunity.

All being well, the provider will confirm acceptance in principle along with its likely fees for the establishment of the pension scheme, pension transfer(s)-in, the property purchase itself and likely ongoing annual administration fees, along with any requirements it has around compulsory property structural surveys / valuations, use of panel Surveyors / Solicitors, appointment of external property managers and so on. Once again, adviser firms can add value by advising clients on the provider market and the potentially significant differential between very prescriptive providers (and the overall costs of these) and those providers that allow clients freedom to choose their own Solicitors, to self-manage properties and so on.

Providing a solution

Having gone through various steps, the adviser firm could well be in a position to make a formal recommendation to the client. That, in turn, could lead to the client making an informed decision on the choice of pension provider to handle the purchase. However, the adviser firm’s involvement need not end at that point; there may be a need for ongoing investment advice (for example, the re-investment of rental income from the property), as well as the need for ongoing overall wealth-planning advice. Although it may be something that adviser firms have never dealt with before, commercial property purchase through pensions might be a valuable service to provide to clients and through which to develop professional connections.

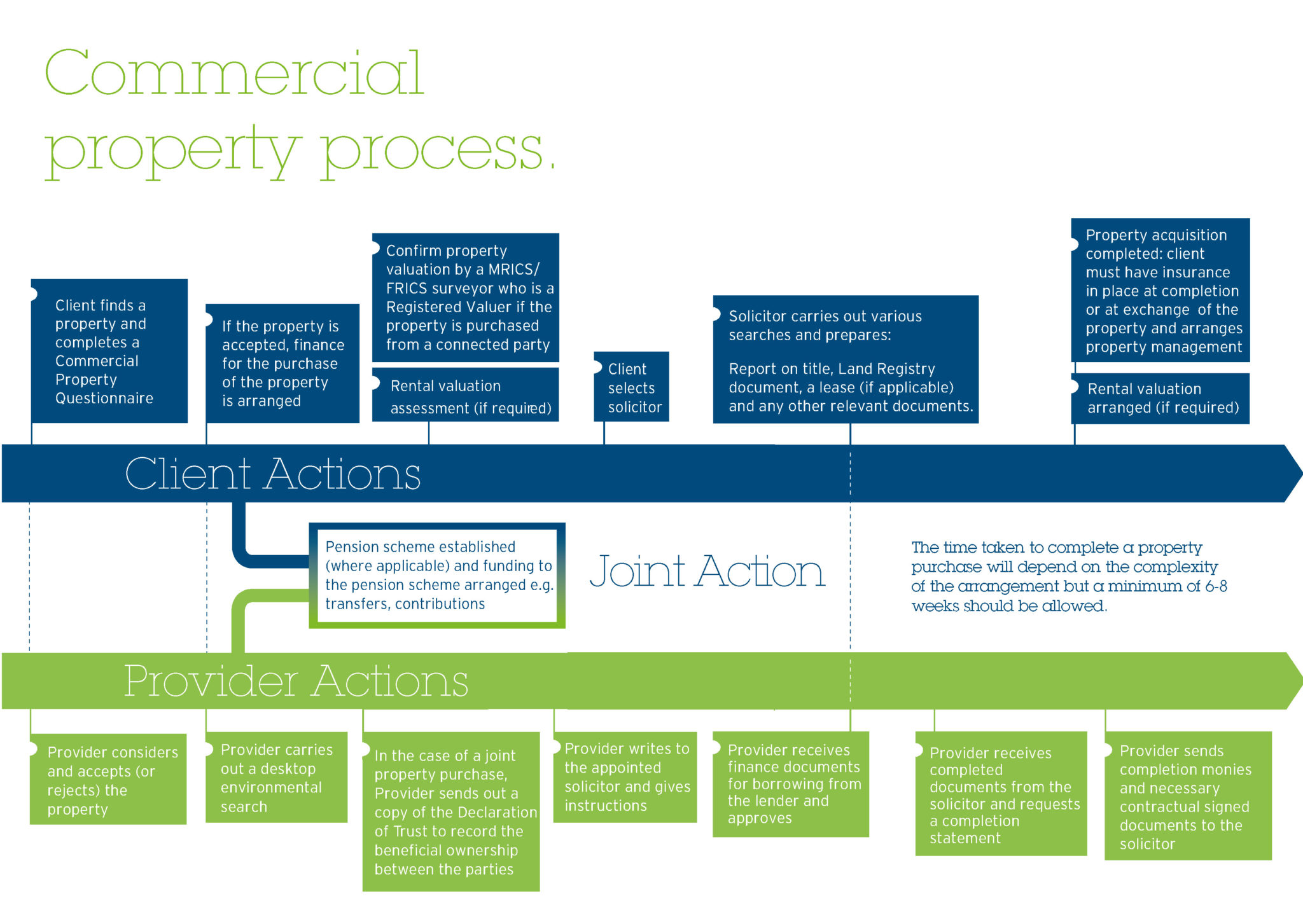

A possible process flowchart is shown below: download it here.